.svg)

OCHO’s Car Insurance Calculator

Figuring out how much car insurance you actually need in 2026 doesn’t have to feel like guesswork. A car insurance calculator takes the mystery out of your next auto insurance policy by letting you plug in your details and see estimated costs before you commit to anything. The calculator takes into account your personal details to provide tailored estimates.

Whether you’re shopping for your first policy, adding a teen driver, or just tired of overpaying, these tools help you understand what you’re really looking at and estimate how much coverage you need.

Car insurance calculators also consider different car insurance coverages, which can affect your estimated costs.

Our Methodology

Numbers are based on real prices that OCHO customers see in your zip code or state. In OCHO's marketplace, customers typically see multiple prices from a variety of insurance carriers we partner with. We use the lowest price shown to each customer to calculate an average across all customers.

- These are initial prices based on preliminary data such as age, marital status, zip code, and coverage type.

- Rates will vary based on other details such as your specific driving record, number of drivers, number of vehicles, etc.

- If the sample size for a given zip code is too small to produce an accurate average (<30 observations), we default to showing statewide averages.

- Down payments are calculated as 25% of the total 6-month policy premium. This is generally a good estimate of what our carriers will require upfront if you buy directly with them instead of through OCHO.

If you indicate you own your vehicle with no loan, we show you state minimum averages, which typically include only liability coverage. If you indicate you lease or finance your vehicle, we show you full coverage averages, which include comprehensive and collision coverage.

What a Car Insurance Calculator Actually Does in 2026

A car insurance calculator is an online tool that estimates your premium and coverage needs before you buy. You enter your information, select the coverage options you want, and the tool generates an estimated cost for a six-month policy based on profiles similar to yours.

Here’s the catch: results are estimates only. The final price always comes from a licensed insurer after they verify your info through motor vehicle reports, claims history databases, and sometimes credit-based insurance scores where legal.Calculators typically use data such as:

- Your ZIP code

- Vehicle details (year, make, model)

- Your driving record

- The coverage amounts you select

These tools pull from large databases, some aggregating data from millions of quotes across dozens of insurers, to predict what you might pay. They’re most useful when comparing multiple insurers side by side instead of checking one company at a time. Think of them as a starting point for smart shopping, not a final answer.

How a Car Insurance Calculator Works Step by Step

Using an auto insurance calculator feels straightforward: you enter your data, pick your coverages, and instantly see estimated six-month premiums, which helps you gauge how much car insurance should cost for your situation. Most tools walk you through the process in under five minutes.

Here’s the catch: results are estimates only. The final price always comes from a licensed insurer after they verify your info through motor vehicle reports, claims history databases, and sometimes credit-based insurance scores where legal.Calculators typically use data such as:

- Your ZIP code

- Vehicle details (year, make, model)

- Your driving record

- The coverage amounts you select

The calculator applies rating factors similar to real insurers. It estimates risk based on territory (urban vs. rural ZIP codes), prior insurance history, at-fault accidents, and tickets. For example, entering details for a 2019 Honda Civic in Dallas, TX, with a clean record might show a six-month estimate around $1,000 to $1,500 for 100/300/50 liability with $500 deductibles.

Many tools assume standard limits by default. If you don’t change anything, you might see estimates based on 100/300/50 liability and $500 comprehensive/collision deductibles. Some calculators also simulate common discounts—safe driver, multi-car, homeowner, or telematics app usage—based on your answers.

The output is typically a price range rather than a single number, accounting for the fact that different insurers charge different car insurance rates for identical profiles.

Key Coverage Decisions Your Calculator Should Guide

A good insurance calculator doesn’t just estimate price; it helps you pick the right coverage limits for your situation by helping you determine how much coverage you need based on your driving habits, risk factors, and personal financial situation. Understanding what you’re buying matters as much as knowing what you’ll pay.

Bodily injury liability and property damage liability form the core of any auto insurance policy. Common limit combinations in 2026 include:

- 50/100/50: Meets minimum requirements in many states but leaves you exposed if you cause a serious car accident

- 100/300/50: Recommended baseline covering $100K per person, $300K total per accident, and $50K property damage

- 250/500/100: Better for urban drivers or anyone with assets to protect; adds 25-50% to premiums but reduces lawsuit risk

Choosing more coverage will increase your premium, but it may offer better protection depending on your needs and risk tolerance.

Comprehensive and collision coverage make sense when you own, lease, or finance a newer vehicle. If you’re driving a financed 2022 Toyota Camry, your lender almost certainly requires both. But for a paid-off 2008 sedan with low vehicle value, dropping these coverages could save you 30-40% on your six-month cost.

Uninsured/underinsured motorist coverage protects you when the other driver has no insurance or not enough. In states like New Mexico or Mississippi, where 25-30% of drivers are uninsured, this coverage is essential.

Deductibles determine how much you pay out of pocket before insurance kicks in. Here’s a practical example:

- $500 deductible: Lower out-of-pocket cost if you file a claim, but higher premium

- $1,000 deductible: Typically reduces your six-month premium by $150-250 (15-20% savings), but you pay more at claim time

Use sliders and drop-downs in calculators to test “what-if” scenarios. See how adding medical payments coverage affects your estimate, or whether it makes sense to carry comprehensive given your car’s age.

Adjusting Coverage for Life Events

Big life events in 2026 should trigger a fresh run of your car insurance calculator. Your coverage needs shift when your circumstances do.

Concrete examples that warrant a new estimate:

- Getting married: Adding a spouse with a clean driving history may drop your rate 5-10% through multi-driver risk pooling

- Adding a partner with recent at-fault accidents: This could spike your premium 30-50%

- Moving from Phoenix to Denver: Different state minimums (Colorado’s 25/50/15 vs. Arizona’s 15/30/10), theft rates, and territory risk scores can shift premiums 20-40%

- Starting a job with a longer commute: Going from a 5-mile local drive to a 50-mile round-trip increases exposure and can raise rates 10-20%

Moving out of state almost always requires a brand-new auto insurance policy. Minimum liability limits, SR-22 rules, and no-fault laws differ significantly. Don’t auto-renew blindly when your life changes—rerun a calculator and see where you stand.

When You Add a New Car or Driver

Buying a new or used car, or adding a teen driver, can change your price more than any other single factor.Real scenarios to consider:

- Adding a 17-year-old in September 2026: Expect premiums to surge 80-150% due to inexperience. The national average for full auto coverage jumps from around $2,324 yearly to $5,000+ with a teen on the policy.

- Replacing a 2013 SUV with a 2024 EV: Advanced safety features might lower rates 10-20%, though higher repair costs for EVs can offset some savings.

- Sharing an older car with a part-time working teen: High deductibles and multi-policy discounts could keep six-month costs under $1,200.

Calculators can estimate how each vehicle in your household affects the premium, but the final rate depends on the actual VIN and complete driving history. Run an estimate before you finalize any purchase so you know whether the insurance costs fit your budget.

What Makes Your Estimate Different from a Real Quote?

Online estimates often don’t match the final price you see when you actually buy. Here’s why.Insurers use third-party data that calculators can only approximate:

- Motor vehicle reports (MVRs): Your complete driving record from the past 3-7 years

- CLUE claims reports: Any insurance claims you’ve filed in the last 7 years

- Prior insurance verification: Gaps in coverage can add surcharges up to 20%

- Credit-based insurance scores: Where legal (not in CA, HI, or MA), these correlate with claims likelihood

Small details matter. A speeding ticket from 2023 that finally shows up on your MVR, or a prior lapse in auto coverage, can shift a six-month premium by 15-30%. When you choose higher limits or add optional coverages like roadside assistance while checking out, your final price will almost always exceed the bare-bones estimate.

Use calculators for directional comparison—which insurer seems cheaper, how much more a newer model might cost to insure—rather than predicting an exact dollar amount. They help you determine where to focus, not what to budget down to the penny.

Many tools assume standard limits by default. If you don’t change anything, you might see estimates based on 100/300/50 liability and $500 comprehensive/collision deductibles. Some calculators also simulate common discounts—safe driver, multi-car, homeowner, or telematics app usage—based on your answers.

The output is typically a price range rather than a single number, accounting for the fact that different insurers charge different car insurance rates for identical profiles.

Which Inputs Have the Biggest Impact on Your Car Insurance Rates?

Although many factors matter, a few major ones drive most of your six-month premium.

Driving record tops the list:

- At-fault accidents in 2024-2025 typically increase rates 40-60% ($500-1,000 extra)

- A DUI from 2022 can add 80-200% to your premium and linger for 5 years

- Good driving history with no incidents earns you a better rate and access to discounts

Vehicle type matters more than most people realize:

- Luxury and high-performance cars (BMW M3, Dodge Charger Hellcat) cost 40-80% more to insure than a Honda Civic or Toyota Corolla

- Theft appeal and repair costs for parts factor heavily into what you pay

Location varies based on where you live:

- Dense urban ZIP codes and high-theft areas command 20-50% higher premiums

- States like Florida and New York historically have averages exceeding $2,500 annually

- Natural disasters risk in your area can affect what you pay for comprehensive coverage

Annual mileage and commuting patterns:

- A 50-mile daily round-trip commute vs. a 5-mile local drive can mean 15-25% higher rates

- More time behind the wheel equals more risk exposure

Credit-based insurance scoring (where legal) correlates strongly with claims likelihood. Drivers with poor scores can face 50-100% higher premiums in states that allow this factor, so it pays to understand how your credit score affects car insurance rates. Availability varies by state, and rules continue to evolve.

Each of these inputs affects how insurers determine your risk profile. Adjust them in a calculator to see which changes save you the most.

Using a Car Insurance Calculator to Compare Policies and Payment Options

Calculators shine when you’re shopping multiple insurers and payment setups at once. Instead of requesting a car insurance quote online from each company individually, you can test scenarios in minutes.

How to compare effectively:

- Run minimum state-required liability (like 25/50/25) against higher recommended limits (100/300/50) back-to-back

- Experiment with different deductibles to see how raising from $500 to $1,000 affects your estimate

- Toggle comprehensive and collision coverage on and off to understand their impact

- Add or remove optional coverages like medical expenses coverage or lost wages protection

Beyond price, calculators help you weigh value: coverage depth, add-ons, and flexibility of payments. The cheapest option isn’t always the best protection, and there are many ways to get cheap car insurance without sacrificing essential coverage. Focus on the best coverage you can reasonably afford—not just the lowest number on the screen.

How OCHO’s Calculator Adds Flexible Payment Plans

At OCHO, we focus on working-class drivers across the U.S. who struggle with big upfront costs. OCHO makes it easier to get free, easy car insurance quotes and flexible payments when a high down payment might otherwise push people to drive uninsured, and that’s a problem we’re here to fix.

When you use OCHO’s calculator, you see not only an estimated six-month premium but also how that cost can be split into smaller installments aligned with your pay cycle, biweekly, or monthly. No surprises.

What makes us different:

- $0 or low down payment options in 2026

- Interest-free financing on the upfront amount similar to pay as you go car insurance with no deposit

- No late fees when you need extra time within your six-month term

- Instant proof of insurance

Our quotes come from multiple partner insurers in real time, so the calculator doubles as a comparison engine plus a payment planner. You see personalized results based on your actual profile, not generic estimates. We help you find coverage options that work and then make paying for them manageable, and you can dig into how OCHO works in more detail if you want specifics.

Credit-Building and Underserved Drivers

Many working-class and underbanked drivers have thin or imperfect credit histories. Traditional insurers often penalize this, making affordable auto coverage feel out of reach, but there are still strategies for getting car insurance with bad credit and keeping it affordable.

On-time payments through OCHO’s financing structure can help build a positive payment history. When you pay consistently, that pattern gets reported to partnering credit bureaus, helping you build the foundation for a better rate down the road.

We see drivers in all situations and stay focused on our mission to serve hardworking drivers:

- Gig workers with irregular paychecks who need flexibility and benefit from pay as you go car insurance

- Families in small towns with few local insurance offices

- People recovering from past financial challenges who need a fresh start

Calculators and flexible payment plans are tools to keep drivers insured and legally on the road. Protect yourself without breaking your budget.

Car Insurance Company Selection

Let's be real here, choosing the right car insurance company isn't just important, it's absolutely crucial. Just as crucial as picking your coverage limits or deductible. With so many insurers out there, each one throwing different auto insurance policies, rates, and service levels at you, you'd be crazy not to do your homework before you commit. Trust us on this one.

Here's where you start: comparing car insurance rates from several companies. And we mean several. Even for the exact same driver and vehicle, insurance rates can swing wildly based on how each company weighs things like your driving record, location, and vehicle type. Using an insurance calculator or auto insurance calculator? Now that's smart thinking. It's your ticket to getting a ballpark car insurance quote from multiple providers all at once. This is how you figure out how much car insurance might actually cost you with each company and which ones are offering the best bang for your buck.

But hold on, don't just fixate on price. Cheap doesn’t always equal better. You need to review the coverage options each insurer brings to the table. Some companies offer way more flexible auto insurance coverage, higher limits, or unique add-ons that'll actually protect you when life throws you a curveball or you get into an accident. Think about this: how easy is it to manage your policy? How painful is it to file a claim? Can you actually get support when you desperately need it? Customer service reviews and digital tools can make or break your entire experience with these people.

Here's the bottom line, and we're going to give it to you straight: the best car insurance company for you is the one that perfectly balances affordable insurance rates, the right coverage, and reliable service that actually shows up when you need it. Take the time to compare—seriously, don't rush this—use those calculators to estimate your real costs, and make absolutely sure the company you choose can deliver the protection and peace of mind you need behind the wheel. Because at the end of the day, that's what this is all about.

When to Rerun Your Car Insurance Calculator in 2026

Car insurance isn’t “set it and forget it.” Your estimate should be updated whenever your life or driving behavior changes.

Specific triggers to rerun your calculator:

- Moving to a new state (coverage requirements and rates vary based on location)

- Switching jobs with a significant commute change

- Paying off an auto loan (you may no longer need to carry comprehensive and collision coverage)

- Adding or removing additional drivers from your policy

- Buying a different car

- After any accident or major claim

Even if nothing major changed, run an annual check-up at each renewal cycle, every six months, to see if better insurance rates or coverage options are available. Insurers adjust pricing constantly, and your profile may qualify for new discounts.

Even if nothing major changed, run an annual check-up at each renewal cycle, every six months, to see if better insurance rates or coverage options are available. Insurers adjust pricing constantly, and your profile may qualify for new discounts.

Don’t auto-renew blindly. Use an online car insurance calculator before locking in your next six-month policy. Tools like OCHO’s let you compare real quotes, test coverage scenarios, and find payment plans that actually fit your budget, and you can always check OCHO’s frequently asked questions if you’re unsure how something works.

Your coverage needs will shift as life happens. Stay ahead of it.

.svg)

FAQs

Car insurance companies rely on sophisticated algorithms that weigh hundreds of factors to calculate your premium. Each company has their own set of parameters. Here’s a list of factors commonly used to determine how much you’ll pay:

Personal Demographics Your age, gender, and marital status significantly impact your rates. Young drivers face the highest premiums due to inexperience and statistically higher accident rates. For example, a 20-year-old driver might pay $5,145 annually on average, while a 40-year-old pays around $2,481 for identical coverage. Married drivers often receive discounts since they're statistically less likely to file claims.

Coverage Choices The type and amount of coverage you select directly affects your premium. Basic state-minimum liability coverage costs much less than comprehensive full coverage that includes collision, comprehensive, uninsured motorist protection, and gap coverage. Higher coverage limits and lower deductibles increase your premium but provide better financial protection.

Driving Record/Motor Vehicle Report (MVR) Your driving history is one of the strongest predictors of future risk. Recent accidents, speeding tickets, DUIs, and other violations can dramatically increase your rates. However, different insurers weigh violations differently - drivers with a recent accident might pay $2,418 annually with one insurer versus $3,094 with another for identical coverage. This is why shopping around after violations is crucial.

Geographic Location Where you live affects your rates in multiple ways. Each state has different minimum coverage requirements, and local factors like crime rates, weather patterns, traffic density, and repair costs influence pricing. We had a customer move just two blocks away into a new ZIP code. That small change alone added $300 to their premium.

Credit Report (in certain states) In some states, insurers may use your credit report to determine your insurance premium. They assess factors like credit score, payment history, and outstanding debt to predict the likelihood of you filing a claim. Believe it or not, but there is a high correlation between credit risk (risk of you missing a payment) and claims risk (risk of you getting into an accident and filing a claim). However, California, Hawaii, and Massachusetts prohibit using credit scores in rate calculations.

Insurance History Your relationship with insurance companies matters. Factors include coverage gaps, recent claims, loyalty discounts for staying with the same insurer, and even which company you're switching from. Continuous coverage demonstrates responsibility and often earns you better rates. A little known fact is that a history of missed payments can raise your insurance rates more than a speeding ticket.

Vehicle Characteristics Your car's make, model, year, safety features, and theft rates in your area all influence pricing. Luxury vehicles, sports cars, and models with high theft rates typically cost more to insure, while vehicles with strong safety ratings and anti-theft features may qualify for discounts.

To get an accurate quote, you'll need basic personal information (name, address, birth date), your driver's license number, vehicle details (year, make, model, VIN), driving history for the past 3-5 years, current insurance information, and desired coverage levels. For our calculator, you only need your age, zip code, vehicle information, and coverage preferences to get a reliable estimate.

There are several ways to lower your car insurance costs:

- Compare quotes from multiple insurers to make sure you’re getting the best deal.

- Maximize available discounts like safe driver, multi-policy, good student, low mileage, or completing a defensive driving course.

- Reduce your annual mileage: the less you drive, the lower your risk of an accident.

- Consider telematics insurance (black box policies): especially useful for younger drivers, as proving safe driving can reduce your premiums over time. Be careful with this service though, it does have the potential to increase your costs if you brake heavily or drive a lot.

- Build up a no-claims bonus: every claim-free year could earn you bigger discounts.

- Choose a lower-risk car: insurance groups vary widely, so check before buying.

- Adjust your coverage: raise your deductible, drop extras you don’t need (like breakdown cover you already have), or scale back coverage on older cars.

- Maintain good credit: insurers often use your credit history when calculating premiums.

- Use our car insurance calculator to see customized ways to save.

- Choose OCHO! We find you our lowest rate when you use our PriceCheck tool. We do this by checking your final rates against the first estimates you selected, so you can rest easy knowing we will always give you the best price.

If you buy your insurance through OCHO, you’ll also benefit from a more human-centered approach than traditional insurers. We make getting insured easier by lowering your down payment and offering flexible payment plans — so you don’t have to stretch your budget to stay protected.

Need more help getting great prices? Check out our tips on low cost car insurance.

Common discounts include safe driver (no accidents/violations), multi-vehicle, multi-policy (bundling home and auto), good student, mature driver (55+), defensive driving course, low mileage, anti-theft devices, safety features, military/federal employee, and loyalty discounts. Some insurers offer usage-based discounts through telematics programs. At OCHO, we help identify all available discounts to maximize your savings.

Coverage needs vary by state requirements and personal financial situation. At minimum, you need your state's required liability limits. However, consider higher limits if you have assets to protect. Full coverage typically includes comprehensive and collision insurance. Evaluate your vehicle's value, your savings, and your risk tolerance. Remember, if you lease your car it’s normally a requirement to have Comp & Collision insurance.

“Full coverage” isn’t an official insurance term, but it’s commonly used to describe a policy that includes liability, comprehensive, and collision coverage. Together, these protect you in several important ways: liability covers damage you cause to other people or their vehicles, comprehensive covers theft and non-collision damage such as weather or vandalism, and collision covers damage to your own car after an accident.

If you finance your vehicle, your lender will almost always require you to carry full coverage. That said, because “full coverage” isn’t a standardized term, what it includes can vary from one insurer to another. It’s also worth remembering that no policy provides 100% protection in every situation, there’s no such thing as being truly “fully covered.”

One more thing to consider: many of our customers don’t have health insurance. For them, adding Medical Payments Coverage (MedPay) is essential, since it can help cover emergency room expenses after an accident.

When comparing quotes, ensure you're comparing identical coverage levels, deductibles, and limits. Look beyond price to consider the insurer's financial stability, customer service ratings, claims handling reputation, and available discounts.

You will also want to pay attention to hidden costs. Sometimes insurers charge extra for things like payment plans and paying by card instead of ACH. Check coverage details carefully - some policies may have exclusions or limitations.

Check our complete guide to free quotes for auto insurance for more details.

Yes, every state except New Hampshire requires minimum liability insurance, though requirements vary significantly. Some states require additional coverage like personal injury protection (PIP) or uninsured motorist coverage. Our calculator factors in your state's requirements based on your zip code to ensure estimates meet legal minimums while showing options for additional protection.

Our calculator provides estimates based on real market data from thousands of actual quotes, making it highly accurate for initial planning purposes. Estimates typically fall within 15-20% of actual quotes, though final premiums may vary based on detailed underwriting factors like specific credit scores, detailed driving records, and individual insurer pricing models. Use our estimates as a reliable starting point for your insurance shopping.

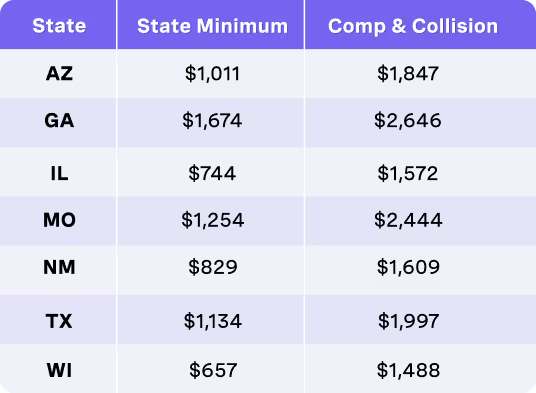

How much car insurance should cost is different for every driver. Rates are based on their personal risk factors. Here's what real OCHO customers pay, on average, to help you set realistic expectations: